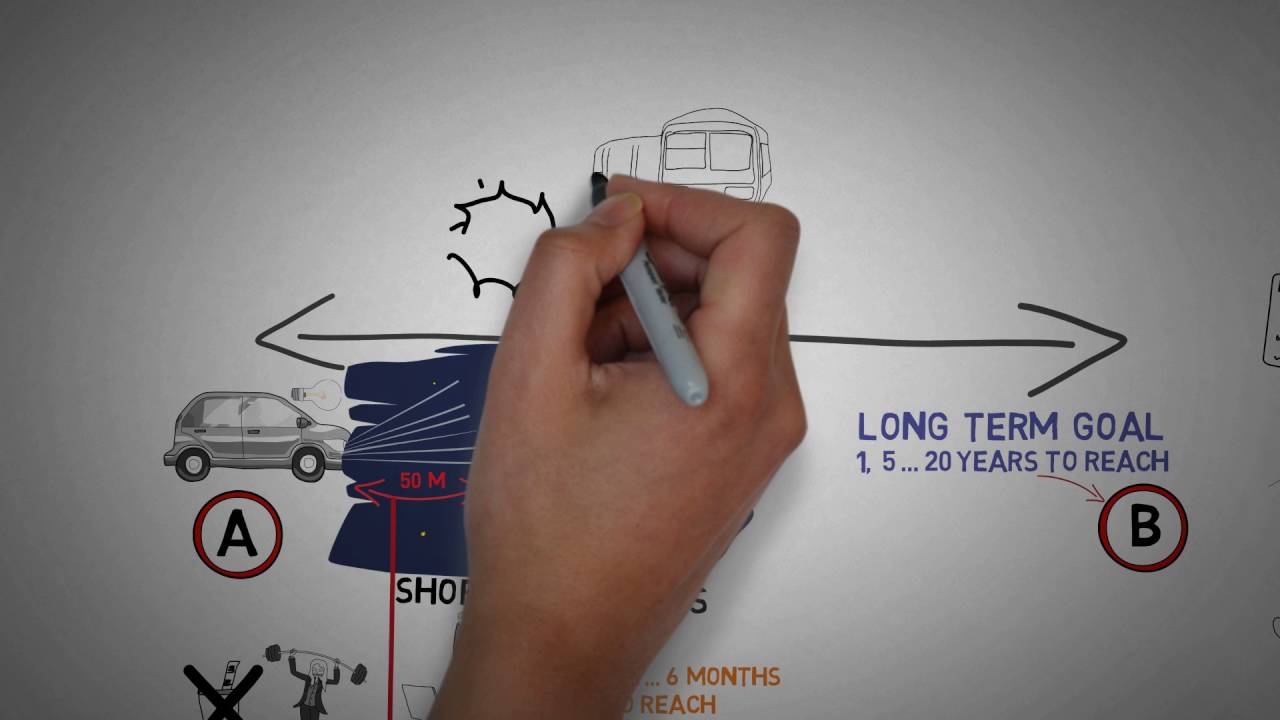

In our journey towards financial stability and prosperity, it is crucial to set clear goals that align with our aspirations and provide a roadmap for success. These financial goals can be broadly categorized into two types: short vs long term goals. While both types are essential, they serve different purposes and require distinct strategies to achieve them.

What Are Short-Term Financial Goals?

Short-Term Financial Planning in 5 Minutes

Short-term financial goals are targets or objectives that can be achieved within a relatively short period, typically within one to three years. These goals are often focused on immediate financial needs, such as saving for a vacation, paying off small debts, building an emergency fund, or making a down payment on a car or a home.

Short-term financial goals play an essential role in maintaining financial stability and setting a solid foundation for achieving long-term financial success. By setting and achieving these short-term goals, individuals can gain a sense of accomplishment and momentum, which can further motivate them to pursue their long-term financial aspirations.

One common short-term financial goal is to build an emergency fund. An emergency fund is a pool of moneyset aside to cover unexpected expenses, such as medical bills, car repairs, or home maintenance. Having an emergency fund provides a financial safety net, ensuring that individuals do not have to rely on credit cards or loans to handle unforeseen circumstances.

Another short-term financial goal is to pay off high-interest debts. This can include credit card debt, personal loans, or outstanding balances on other types of loans. By prioritizing debt repayment, individuals can reduce their overall debt burden, save moneyon interest payments, and improve their financial well-being.

Saving for specific purchases or experiences is also a common short-term financial goal. Whether it's a dream vacation, a new gadget, or a home improvement project, setting aside funds specifically for these goals allows individuals to enjoy the satisfaction of achieving them without going into debt.

It is important to note that short-term financial goals should be realistic and achievable within the chosen timeframe. Setting goals that are too ambitious or unrealistic can lead to frustration and disappointment. It is crucial to assess one's current financial situation and set goals that are aligned with their income, expenses, and financial capabilities.

What Are Long-Term Financial Goals?

Long-term financial goals are targets or objectives that require a more extended period to achieve, typically spanning several years or even decades. These goals are often focused on major life eventsor financial milestones, such as retirement planning, purchasing a home, saving for children's education, or achieving financial independence.

One of the most significant long-term financial goals for many individuals is retirement planning. Planning for retirement involves setting aside funds that will provide income and financial security during the post-employment years. This can include contributing to retirement accounts like 401(k)s or Individual Retirement Accounts (IRAs) and making investments that will grow over time.

Another common long-term financial goal is homeownership. Saving for a down payment, improving credit scores, and obtaining a mortgage are important steps towards purchasing a home. Long-term planning and budgeting are necessary to accumulate the necessary funds and ensure that homeownership is sustainable in the long run.

Saving for children's education is also a crucial long-term financial goal for many parents. With the rising costs of higher education, starting early and regularly contributing to education savings accounts, such as 529 plans, can help alleviate the burden of student loans and provide children with more opportunities for their future.

Long-term financial goals may also include achieving financial independence, starting a business, or building a substantial investment portfolio. These goals often require careful planning, consistent savings, and wise investment decisions to generate wealth and secure financial freedom.

Long term and short term planning animated

How To Prioritize Goals

With various short-term and long-term financial goals, it's important to prioritize them based on their importance and feasibility. Here are some steps to help prioritize your goals:

- Identify and List Your Goals -Start by making a comprehensive list of all your financial goals, both short-term and long-term. Be specific about each goal and assign a timeframe for achieving them.

- Determine the Significance -Assess the importance and impact of each goal on your life. Consider factors such as financial security, personal fulfillment, and long-term well-being. Rank your goals based on their significance.

- Consider Timeframe -Differentiate between short-term and long-term goals. Identify which goals need immediate attention and which ones can be pursued over a more extended period. This will help you allocate resources effectively.

- Evaluate Financial Feasibility -Assess the financial feasibility of each goal. Determine how much you need to save or invest to achieve them. Consider your income, expenses, and other financial obligations. Be realistic about what you can afford.

- Balance Between Goals -Strike a balance between short-term and long-term goals. While it's important to focus on immediate needs, don't neglect the long-term objectives. Allocate resources in a way that allows progress towards both types of goals.

- Review and Adjust -Regularly review and reassess your goals. Circumstances may change, and priorities can shift over time. Adjust your goals and strategies accordingly to stay on track and adapt to new situations.

Remember that prioritizing goals is a personal decision and can vary from person to person. It's essential to align your goals with your values, aspirations, and financial circumstances.

How Do You Budget For Future Expenses?

Budgeting for future expenses is a crucial aspect of financial planning. By allocating funds towards future goals and anticipated expenses, individuals can better manage their finances and work towards achieving their desired outcomes. Here are some steps to help you budget for future expenses:

- Track Your Current Expenses -Start by understanding your current spending patterns. Track your expenses over a few months to get a clear picture of where your money is going. Categorize your expenses, such as housing, transportation, food, entertainment, and savings.

- Determine Future Expenses -Identify upcoming expenses or financial goals that you need to budget for. This can include events like weddings, vacations, major purchases, or anticipated life changes such as starting a family or purchasing a home.

- Estimate Costs -Research and estimate the costs associated with your future expenses. Consider factors such as inflation, taxes, and any additional expenses that may arise. Be as accurate as possible to ensure your budget is realistic.

- Create a Budget -Based on your income and current expenses, develop a budget that incorporates your future expenses. Allocate funds towards each category, including savings for future goals. Ensure that your total expenses do not exceed your income.

- Automate Savings -Set up automatic transfers or contributions to separate savings accounts or investment vehicles specifically designated for future expenses. Automating savings helps you stay disciplined and ensures that funds are consistently set aside for your goals.

- Monitor and Adjust -Regularly review your budget and track your progress. Monitor your expenses and savings to ensure that you're on track towards meeting your future financial goals. Adjust your budget as needed to accommodate any changes in circumstances or priorities.

Budgeting for future expenses requires discipline and conscious decision-making. It's essential to strike a balance between enjoying the present and preparing for the future. By creating a realistic budget and consistently sticking to it, you can effectively allocate resources towards future expenses and work towards achieving your financial objectives.

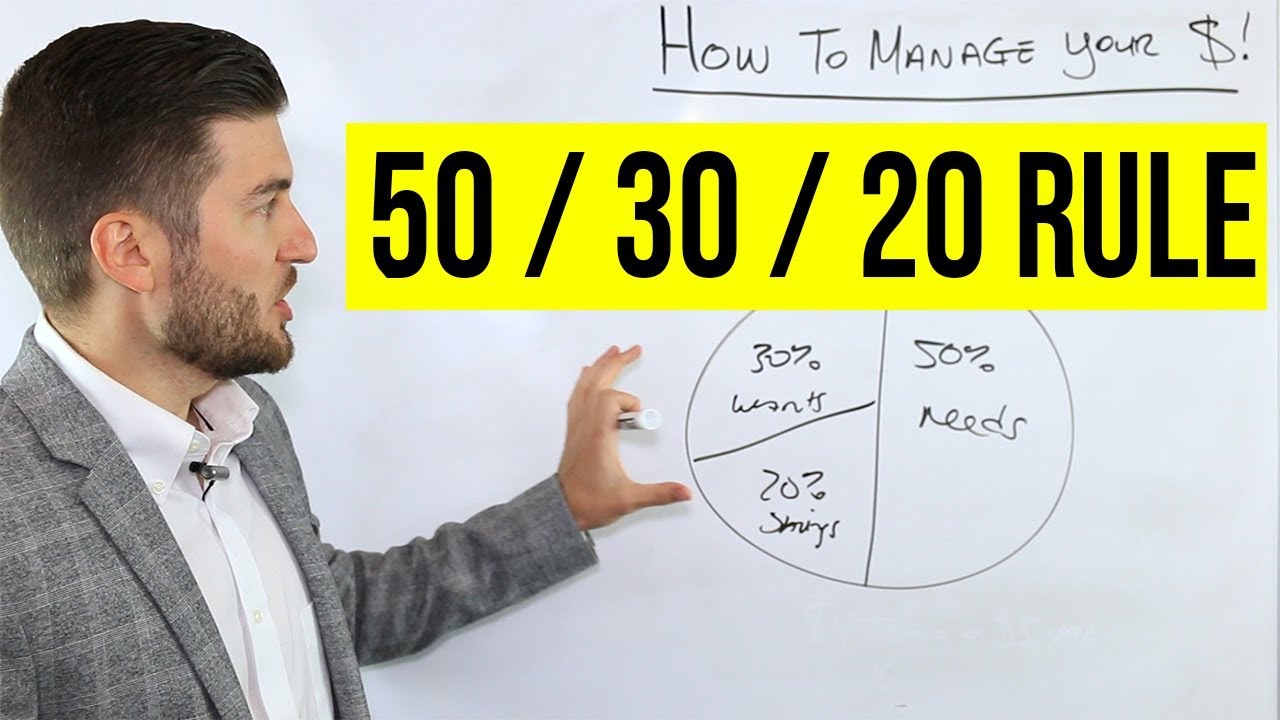

How To Manage Your Money (50/30/20 Rule)

Where Should I Invest My Savings?

Determining where to invest your savings depends on various factors, including your financial goals, risk tolerance, time horizon, and investment knowledge. Here are some investment options to consider:

- Stocks -Investing in individual stocks can offer potential high returns but also carries higher risks. It requires research and analysis to select individual companies. Consider diversifying your stock portfolio to reduce risk.

- Bonds -Bonds are debt securities issued by governments or corporations. They provide fixed interest payments over a specific period, making them relatively less risky than stocks. Bonds can provide income and stability to a portfolio.

- Mutual Funds -Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. They are managed by professionals and offer instant diversification, making them suitable for beginners.

- Exchange-Traded Funds (ETFs) -ETFs are similar to mutual funds but trade on stock exchanges like individual stocks. They offer diversification and lower costs compared to mutual funds. ETFs can track indexes or specific market sectors.

- Real Estate -Investing in real estate can provide rental income and potential property appreciation. This can be done by purchasing properties directly or investing in real estate investment trusts (REITs) or real estate crowdfunding platforms.

- Retirement Accounts -Contributing to retirement accounts like 401(k)s or IRAs offers tax advantages and long-term growth potential. Take advantage of employer matching contributions if available.

- Diversification -Diversifying your investment portfolio is crucial to manage risk. Allocate your savings across different asset classes, such as stocks, bonds, and real estate, to spread risk and potentially enhance returns.

- Consult a Financial Advisor -If you're unsure about investment options or need personalized advice, consider consulting a financial advisor. They can assess your financial situation, risk tolerance, and goals to provide tailored investment recommendations.

Remember that investing involves risk, and past performance is not indicative of future results. It's important to educate yourself about investment options, diversify your portfolio, and regularly review your investments to ensure they align with your financial goals.

People Also Ask

How Can I Track My Progress Towards My Financial Goals?

To track your progress towards your financial goals:

- Define specific milestones.

- Monitor your income and expenses.

- Review and adjust regularly.

How Can I Make My Budget More Flexible To Accommodate Unexpected Expenses?

To make your budget more flexible for unexpected expenses:

- Build an emergency fund.

- Include a miscellaneous or "buffer" category.

- Review and adjust regularly.

How Can I Balance Saving For Retirement With Other Financial Goals?

To balance saving for retirement with other financial goals:

- Prioritize retirement savings.

- Allocate a portion of your income to other goals.

- Review and adjust as your circumstances change.

Conclusion

In conclusion, setting short vs long term goals provides a roadmap for achieving financial stability and success. Prioritizing goals, budgeting for future expenses, and making informed investment decisions can help you make progress toward your desired financial outcomes. Remember to regularly review and adjust your goals and strategies to stay on track and adapt to changing circumstances.