Are you curious about your creditworthiness and how lenders evaluate your borrowing potential? If so, understanding your FICO scoreis crucial. Your FICO score is a three-digit number that serves as a key determinant in loan approvals, interest rates, and credit decisions. In this comprehensive guide, we will delve into the intricacies of FICO scores, exploring what they are, how they work, and how you can improve them.

When it comes to assessing your creditworthiness, the Fair Isaac Corporation (FICO) score is the industry standard. Lenders across the globe rely on this credit scoring model to evaluate the risk associated with extending credit to borrowers. A FICO score provides a standardized approach to evaluating creditworthiness, allowing lenders to make informed decisions based on a borrower's credit history.

In this guide, we will address a range of topics related to FICO scores, helping you navigate the complexities of credit evaluation. From understanding the FICO score range and how FICO scores work to exploring strategies for improving your score, we have you covered.

To begin our journey, let's explore the fundamentals of FICO scores.

What Is A FICO Score?

A FICO score is a credit scoring model used by lenders to assess an individual's creditworthiness. It is a three-digit number that represents a borrower's credit risk based on their credit history. FICO scores range from 300 to 850, with higher scores indicating lower credit risk.

What Is The FICO Score Range?

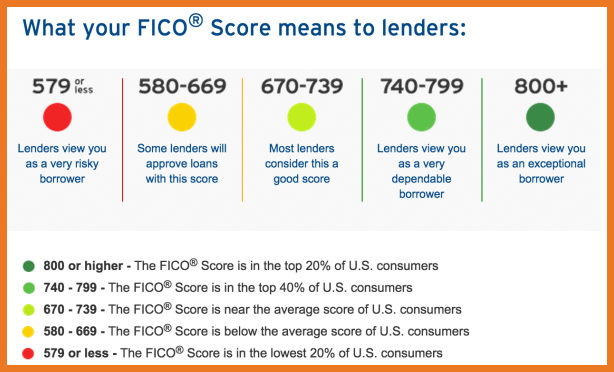

The FICO score range categorizes credit scores into different tiers to assess creditworthiness. The range spans from 300 to 850, and the classification is as follows:

- Exceptional- Scores of 800 and above

- Very Good- Scores of 740-799

- Good- Scores of 670-739

- Fair- Scores of 580-669

- Poor- Scores below 579

Lenders use the FICO score range to evaluate credit applications and determine the terms of credit extended to borrowers.

How FICO Scores Work

FICO scores are calculated using various factors from an individual's credit report. These factors include payment history, amounts owed, length of credit history, credit mix, and new credit. Each factor contributes differently to the overall FICO score calculation.

- Payment history- Reflects the borrower's track record of making on-time payments.

- Amounts owed- Considers the borrower's outstanding debt compared to their available credit.

- Length of credit history- Reflects how long the borrower has been using credit.

- Credit mix- Considers the types of credit accounts the borrower has.

- New credit- Analyzes the borrower's recent credit inquiries and new accounts.

These factors are analyzed to determine the borrower's credit risk and calculate their overall creditworthiness.

How Much FICO Score Ranges

The FICO score range provides lenders with an indication of a borrower's creditworthiness. The range spans from 300 to 850, and the score classification helps lenders evaluate credit applications. Here is a breakdown of the FICO score ranges:

- Exceptional- Scores of 800 and above - Indicate very low credit risk.

- Very Good- Scores of 740-799 - Suggest low credit risk.

- Good- Scores of 670-739 - Considered satisfactory by lenders.

- Fair- Scores of 580-669 - Suggest higher credit risk.

- Poor- Scores below 579 - Indicate high credit risk.

The FICO score range provides borrowers with a general idea of where they stand in terms of creditworthiness and helps them understand the potential impact on their borrowing capabilities.

How To Improve Your FICO Score

Improving your FICO score is possible with careful financial management and responsible credit behavior. Here are some strategies to help you improve your FICO score:

- Pay your bills on time -Consistently making on-time payments is crucial for improving your FICO score. Late payments can negatively impact your score, so it's essential to prioritize timely payments.

- Reduce your debt -Lowering your overall debt can positively impact your FICO score. Focus on paying down high-interest debts first and consider budgeting and financial planning strategies to manage your debt effectively.

- Keep credit card balances low -High credit card utilization can harm your FICO score. Aim to keep your credit card balances below 30% of your credit limit to demonstrate responsible credit utilization.

- Maintain a mix of credit -Having a diverse mix of credit accounts, such as credit cards, loans, and mortgages, can positively impact your FICO score. It shows that you can handle different types of credit responsibly.

- Avoid opening unnecessary accounts -Opening multiple new accounts within a short period can negatively impact your FICO score. Only apply for credit when necessary and consider the potential impact on your creditworthiness.

- Regularly review your credit report -Checking your credit report regularly allows you to identify any errors or inaccuracies that could be affecting your FICO score. Dispute any incorrect information with the credit bureaus to have it corrected promptly.

- Be patient -Improving your FICO score takes time and consistent effort. Focus on practicing responsible credit behavior, and over time, you'll see positive changes in your creditworthiness.

By following these strategies, you can take control of your credit health and work towards improving your FICO score over time.

How Is A FICO Score Calculated?

How a FICO Credit Score Is Determined (2020 update) | Continuing Feducation

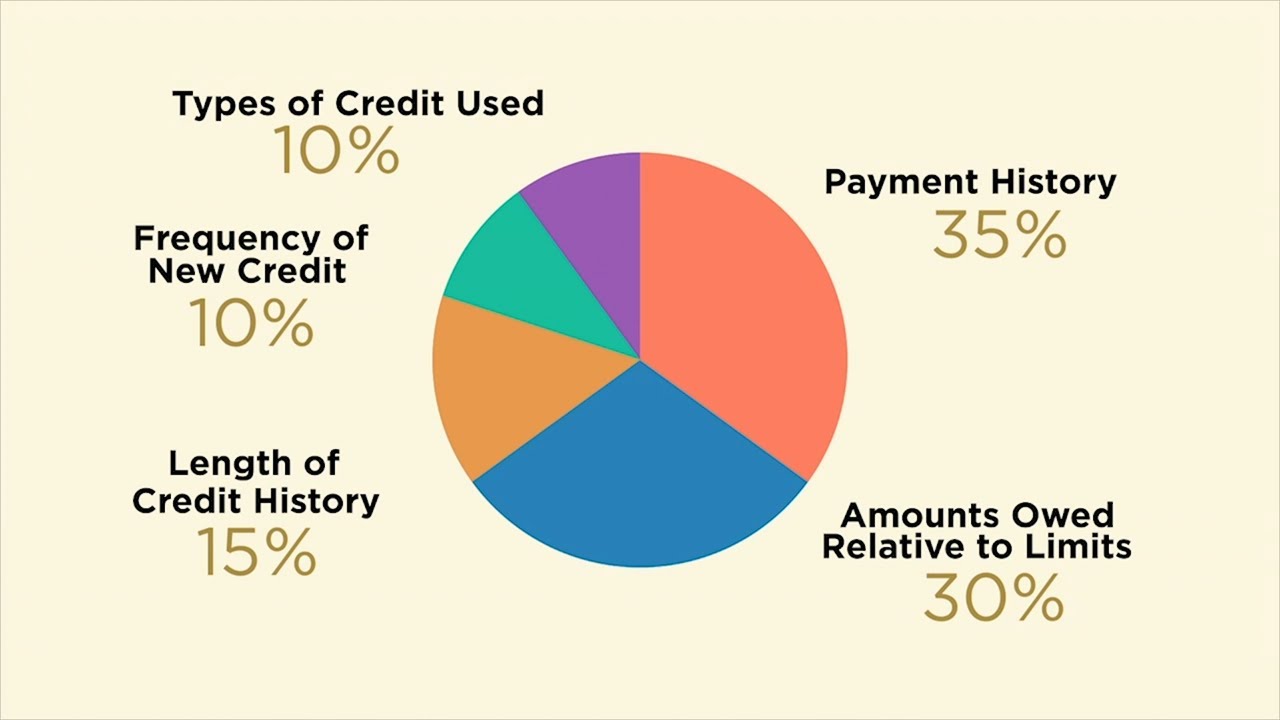

FICO scores are calculated using a complex algorithm developed by the Fair Isaac Corporation. Although the exact details of the algorithm are proprietary and not publicly disclosed, the general factors and their weights in calculating the score are known.

Payment history, amounts owed, length of credit history, credit mix, and new credit are the primary factors considered in FICO score calculations. However, the precise weightings of these factors may vary depending on individual credit profiles and other variables.

- Payment history,35% - Your track record of making timely payments plays a significant role in your FICO score calculation.

- Amounts owed,30% - The ratio of your credit card balances to your credit limits, also known as credit utilization, is a crucial factor.

- Length of credit history,15% - The length of time you have held credit accounts contributes to your FICO score.

- Credit mix,10% - The variety of credit accounts you have can impact your FICO score.

- New credit, 10% - Opening multiple new accounts or having numerous credit inquiries can lower your FICO score.

The algorithm analyzes these factors in conjunction with the information from an individual's credit report to produce a FICO score. The resulting score serves as a numerical representation of the borrower's creditworthiness and helps lenders assess the risk associated with extending credit.

It's important to note that FICO scores are not the only credit scoring models used by lenders. Other credit scoring models, such as VantageScore, may also be utilized. However, FICO scores remain widely adopted and recognized as the industry standard in credit evaluation.

What Is A Good FICO Score?

A good FICO score is typically considered to be 670 or above. With a good score, borrowers are likely to be approved for credit and offered favorable interest rates. However, higher scores, such as those in the exceptional or very good range, can provide even better borrowing opportunities and lower interest rates.

The specific interpretation of a good FICO score may vary slightly among lenders and the type of credit being sought. It's important to keep in mind that each lender may have its own criteria for evaluating creditworthiness beyond the FICO score alone.

Which FICO Score Do Mortgage Lenders Use?

Mortgage lenders typically use FICO scores specifically tailored for mortgage lending. These versions of the FICO scoring model, such as FICO Score 2, FICO Score 4, or FICO Score 5, place more emphasis on factors relevant to mortgage lending, such as payment history for mortgage loans.

The choice of the FICO scoring model version may vary among mortgage lenders. It's crucial to consult with your lender to understand which version they utilize and how it may impact your mortgage application.

What Affects Your FICO Score?

Several factors can influence your FICO score:

- Payment history -Your track record of making timely payments plays a significant role in your FICO score calculation. Late payments, defaults, and bankruptcies can have a detrimental impact.

- Credit utilization -The ratio of your credit card balances to your credit limits, also known as credit utilization, is another important factor. High credit card balances relative to your available credit can lower your FICO score.

- Length of credit history -The length of time you have held credit accounts contributes to your FICO score. A longer credit history can be advantageous for your score, as it provides more data for evaluation.

- Credit mix -The variety of credit accounts you have, such as credit cards, loans, and mortgages, can impact your FICO score. A well-managed mix of credit types can positively influence your score.

- New credit - Opening multiple new accounts within a short period or having numerous credit inquiries can lower your FICO score. It suggests higher credit risk and can be perceived as a sign of financial instability.

It's important to note that while these factors significantly influence your FICO score, individual circumstances and credit histories can vary. Additionally, the weight assigned to each factor may differ depending on the individual's credit profile.

FICO Score Vs. Credit Score

FICO Score vs Credit Score [What's the Difference?]

The terms "FICO score" and "credit score" are often used interchangeably. However, it's essential to understand that the FICO score is just one type of credit score available. Other credit scoring models, such as VantageScore, also exist.

Different lenders may use different credit scoring models to evaluate credit applications. While FICO scores are widely adopted, some lenders may have a preference for alternative scoring models depending on their specific requirements or industry standards.

It's important to be aware of the scoring model used by the lender when applying for credit to understand how it may impact your credit evaluation.

FICO Score Vs. VantageScore

VantageScore vs FICO - Credit Score Ranges (EXPLAINED)

VantageScore is another widely used credit scoring model, jointly developed by the three major credit bureaus: Experian, Equifax, and TransUnion. While VantageScore and FICO scores both assess creditworthiness, there are some differences between the two.

Although both scoring models consider similar factors such as payment history and credit utilization, they may weigh these factors differently. As a result, the scores generated by each model may vary.

Lenders may have a preference for one scoring model over the other, depending on their internal policies and credit evaluation practices. It's essential to understand which model your lender uses and how it may impact your credit assessment.

How Do I Get A FICO Score?

To obtain your FICO score, you can follow these steps:

- Check with your financial institution - Some banks and credit card issuers provide FICO scores as a benefit to their customers. Contact your bank or credit card issuer to inquire if they offer this service.

- Purchase your FICO score -You can purchase your FICO score directly from the Fair Isaac Corporation or from myFICO.com, the official FICO website.

- Credit monitoring services -Several credit monitoring services offer access to FICO scores as part of their subscription packages. These services allow you to monitor your credit report and score regularly.

Remember that you are entitled to a free credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year. While the credit report does not include your FICO score, reviewing it can provide valuable insights into your credit history and help you identify areas for improvement.

People Also Ask

What Is A Good FICO Score?

A good FICO score is typically considered to be in the range of 670 to 739. Although ranges may vary slightly depending on the credit scoring model, this range generally indicates a good credit standing. It suggests that individuals within this range are likely to be approved for credit and offered favorable terms and interest rates.

Who Uses FICO Scores?

Lenders are the primary users of FICO Scores. When you apply for a mortgage, auto loan, credit card, or any new line of credit, the bank or lender will likely assess your FICO Score. Lenders rely on FICO Scores to make informed decisions about credit approvals, loan terms, and interest rates. By reviewing your FICO Score, lenders can evaluate your creditworthiness and assess the level of risk associated with extending credit to you.

What Is The Most Important Part Of A FICO Score?

The most important factor of your FICO Score is your payment history. Whether you consistently pay your bills on time or have a history of late payments significantly impacts your credit score. In fact, payment history contributes the most weight to your FICO Score calculation, accounting for 35% of the overall score.

Conclusion

In conclusion, understanding your FICO score is essential for managing your credit and making informed financial decisions. By knowing how FICO scores are calculated, what factors affect them, and how toimprove them, you can take proactive steps to build and maintain a strong credit profile. Monitoring your FICO score regularly and using it as a benchmark will empower you to navigate the world of credit more effectively.